( ESNUG 593 Item 05 ) --------------------------------------------- [04/13/23]

Subject: Snarkies on Shi's vs. Jay's actual 2022 revenue data and analysis

Editor's Note: Every time I publish, the readers send me these

concise replys that are sometimes insightful, but are more often

cynical -- which is why I call them "snarkies". Enjoy. - John

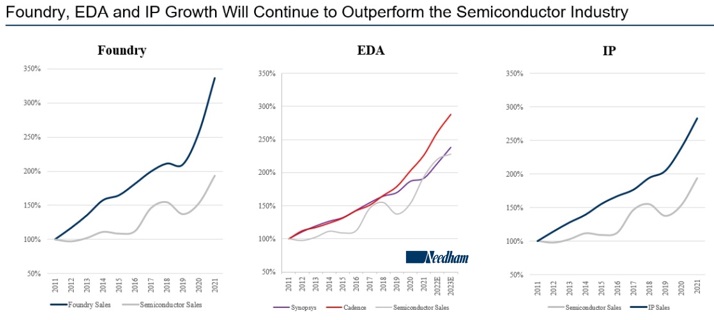

Charles' DAC'22 talk was deep into semiconductor cycles, wafer shipments,

chip manufacturing costs, CapEx spending by TSMC-Intel-UMC-GF-&-SMIC,

cost-per-wafer, cost-per-xistor, cost-per-bare-die, rising wafer costs,

Moore's Law not scaling, N20-N16-N10-N7-N5 costs to Apple, reticle limits,

chiplets, 2D going to 2.5D/3D, Cadence vs. Ansys, TSMC N3E FinFlex not

scaling, Qualcomm's ASP vs. Apple's costs, "chip design will go from a

few to many", "design democratization is coming..."

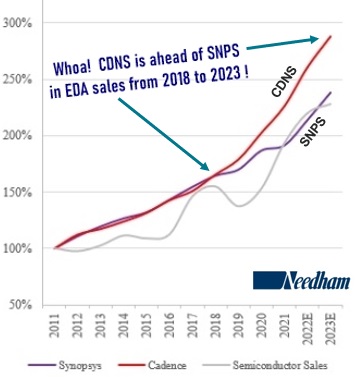

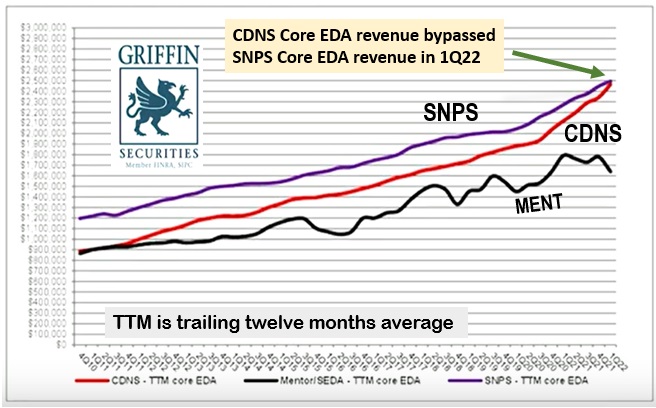

And then Charles Shi closed his talk with a shocking slide:

Zoom in and you'll see what Cooley (my added markings) saw:

Charles (very quietly) declared that CDNS (line in red) has been crushing

SNPS in pure EDA sales since 2018 -- and Charles predicted in his graph that

Anirudh will keep on crushing SNPS in EDA even in 2023!

That is, Charles Shi had quietly crowned Anirudh the King of Core EDA.

- Two Wall St. analysts crown Anirudh as 2022 King of EDA

---- ---- ---- ---- ---- ---- ----

Shi's analysis has Anirudh besting Aart in pure EDA revenue in 2018.

Jay's analysis has Anirudh besting Aart in pure EDA revenue in 2022.

That's a four year difference.

Since Shi is new, I would like to know how he came up with his analysis.

---- ---- ---- ---- ---- ---- ----

I noticed that change in Cadence digital implementation around 2018, too.

---- ---- ---- ---- ---- ---- ----

2018 is when Anirudh took full control of Cadence, yes?

---- ---- ---- ---- ---- ---- ----

Why didn't Shi make this news the major point of his presentation?

Did Charles not understand how significant Cadence passing Synopsys was?

---- ---- ---- ---- ---- ---- ----

I like Shi's percent change from 2011 analysis better than Jay's

absolute numbers.

Because of arbitrary revenue recognition issues, Y-to-Y percent change

is much harder to fudge than absolute numbers are.

---- ---- ---- ---- ---- ---- ----

That 2018 tipping point that Shi has is wrong.

From Jay's data the true tipping point was in 2022.

---- ---- ---- ---- ---- ---- ----

When we finally dropped PrimeTime for Tempus in 2020 for golden

signoff, that made us a Cadence backend and Mentor Calibre DRC house.

Prior to 2020 we were Synopsys-Cadence-Mentor.

---- ---- ---- ---- ---- ---- ----

Going 2011 baseline and measuring percent change is from there

is an interesting way of looking at this.

---- ---- ---- ---- ---- ---- ----

Why 2011?

What event happened then that Shi chose 2011 as a starting point?

---- ---- ---- ---- ---- ---- ----

(And my spies tell me that Jay Vleeschhouwer's DAC'22 presentation also had

a similar slide showing CNDS EDA sales had bypassed SNPS EDA sales in

roughly the same time frame -- but I don't have a pic of that slide.)

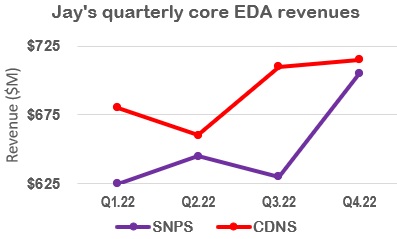

JAY'S CONFIRMATION: Since I couldn't get a screenshot of Jay's DAC'22 slides

on this, I did the next best thing -- I pawed through Jay's 2022 quarterly

reports on the individual Earnings Calls for SNPS and CDNS to see what Jay

saw for Core EDA revenues (i.e. no IP, no HW, just SW) for each company.

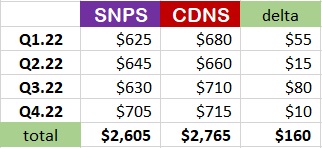

SNPS 22Q1: :############################### $625M

CDNS 22Q1: :################################## $680M ($55M more)

SNPS 22Q2: :################################ $645M

CDNS 22Q2: :################################# $660M ($15M more)

SNPS 22Q3: :################################ $630M

CDNS 22Q3: :#################################### $710M ($80M more)

SNPS 22Q4: :################################## $705M

CDNS 22Q4: :#################################### $715M ($10M more)

So for FY2022, Jay saw CDNS $160M ahead of SNPS in core EDA revenues.

That is, Anirudh was 6% ahead of Aart in core EDA for 2022.

- Two Wall St. analysts crown Anirudh as 2022 King of EDA

---- ---- ---- ---- ---- ---- ----

---- ---- ---- ---- ---- ---- ----

---- ---- ---- ---- ---- ---- ----

Editor's Note: I added markings to better explain Jay's slide data. - John

Here's Jay's DAC slide you asked for. Jay only did trailing twelve months

analysis so his latest data at DAC'22 was only for the 1st quarter on 2022.

The Vleeschhouwer data for 2Q22, 3Q22, 4Q22 and his $160M delta just later

confirmed what he was saying at DAC.

---- ---- ---- ---- ---- ---- ----

"Our new analysis shows in the first quarter of 2022 that Cadence has

surpassed Synopsys revenue in Core EDA."

- Jay Vleeschhouwer, at DAC 2022

---- ---- ---- ---- ---- ---- ----

What you're missing, John, is that while Cadence is growing in Core EDA,

Synopsys is growing in IP.

---- ---- ---- ---- ---- ---- ----

I liked that Shi's observation was confirmed by Jay.

What's interesting is how these two came to the same conclusion (of CDNS

passing SNPS in Core EDA) from two different paths.

---- ---- ---- ---- ---- ---- ----

If it was one quarter that had a bump, that would be a fluke.

The fact that all quarters were ahead and that two of the four CDNS quarters

were strongly ahead ($55M and $80M) shows it is an actual tipping point.

---- ---- ---- ---- ---- ---- ----

I wouldn't call "no IP, no HW, just SW" as "Core EDA".

I would just call it EDA.

That other stuff (IP & HW) is what my wife would call "accessories".

---- ---- ---- ---- ---- ---- ----

Thanks for pulling out those data points from Jay's reports.

I follow Jay purely because his grainular analysis is far more truthful

than any 10-K or set of 10-Qs.

---- ---- ---- ---- ---- ---- ----

I think you're overstating this story, John.

Being "6% ahead" is being effectively tied with this type of data.

---- ---- ---- ---- ---- ---- ----

$2,605 M plus $2,765 M equals $5,370 M

$160 M divided by $5,370 M equals 2.98%.

A 3 percent difference is the correct analysis.

A tie.

---- ---- ---- ---- ---- ---- ----

Matching Aart doesn't make Anirudh a king.

It makes Anirudh one of Aart's equals. Nothing more.

---- ---- ---- ---- ---- ---- ----

I think it's entertaining how a $160 million lead is "big news" in EDA.

The enterprise SW market is ~$400 billion. That's billion with a "B".

$160 million is the what the enterprise SW companies spend every year

on 3M Post-It sticky note pads.

---- ---- ---- ---- ---- ---- ----

---- ---- ---- ---- ---- ---- ----

---- ---- ---- ---- ---- ---- ----

"Growth contest between SNPS and CDNS is still a tie.

Investors like to ask us: between SNPS and CDNS, which one will

grow faster over the longer term? Our answer has consistently

been "it is hard to tell". The SNPS print tells us that SNPS' EDA

growth may be showing signs of underperformance, but SNPS' higher

mix and stronger growth of IP is lifting its overall growth to

a simliar level as CDNS.

Over a longer term, both companies should do similarly if not

equally well."

- Charles Shi, SNPS 2Q22 Needham report (05/19/2022)

- Two Wall St. analysts crown Anirudh as 2022 King of EDA

---- ---- ---- ---- ---- ---- ----

That's the most concise and best summary of why investing in public EDA

stocks has paid off so well for me over the years.

---- ---- ---- ---- ---- ---- ----

Shi is spot on with this

---- ---- ---- ---- ---- ---- ----

Three years ago Thanksgiving dinner I had a relative ask me should

he invest in Synopsys or Cadence for the long term?

Which one to choose?

I told him either one. Either or both are good.

---- ---- ---- ---- ---- ---- ----

I wonder what Shi thinks about Mentor and Siemens EDA.

Can you ask him?

---- ---- ---- ---- ---- ---- ----

A new guy can sometime see the things that we forgot were there.

---- ---- ---- ---- ---- ---- ----

Related Articles

Cooley's two new policies of Radical Laziness and Radical Honesty

Snarkies on Charles Shi, Jay Vleeschhouwer, Rich Valera, Gary Smith

Snarkies on Shi's vs. Jay's actual 2022 revenue data and analysis

Snarkies on CDNS/SNPS margins, backlog, growth and Anirudh/Fister

Snarkies on Anirudh 2023 vs. Synopsys.ai, ChatGDP, and chiplets

Join

Index

Next->Item

|

|