( ESNUG 593 Item 02 ) --------------------------------------------- [02/23/23]

Subject: Two Wall St. analysts (quietly) crown Anirudh as 2022 King of EDA

THE NEW NEEDHAM ANALYST: Whenever I meet a new Wall St. analyst (like when

the new guy Charles Shi replaced Rich Valera at Needham) I like to check

them out. See if they bring any real skills to evaluating EDA stocks. Or

are they just sock puppets who parrot whatever the EDA companies tell them?

In my book, a new EDA Wall St. analyst is to be respected if he (or she) has

either amazing accounting/finance/investigative skills to cut through the

B.S. that the public EDA companies spout on their quarterly Earnings Calls

and/or financials (like Jay Vleeschhouwer) ...

Or he (or she) has years of chip design and/or chip verification experience

to -- again -- cut through the B.S. that the public EDA companies spout on

their quarterly Earnings Calls and/or financials (like Gary Smith).

At his introductory talk at DAC'22 in San Francisco, I was very pleasantly

surprised to learn that Charles Shi was a foundry guy with 6 years direct

hands on semi experince at Applied Materials (AMAT)!!!

"Holy crap! AMAT!!! This new Shi guy speaks fluent Chinese, he covers

TSMC stock, and he is schooling us in EDA from a foundry perspective!!!"

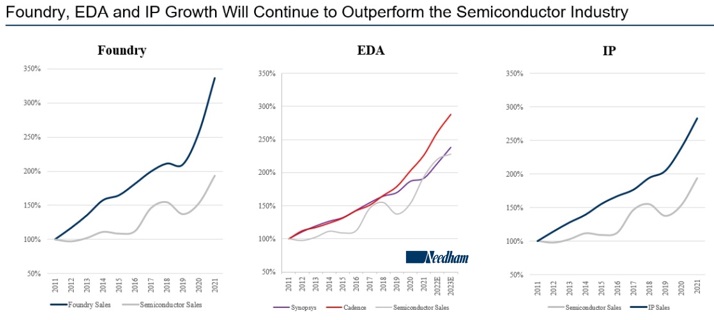

Charles' DAC'22 talk was deep into semiconductor cycles, wafer shipments,

chip manufacturing costs, CapEx spending by TSMC-Intel-UMC-GF-&-SMIC,

cost-per-wafer, cost-per-xistor, cost-per-bare-die, rising wafer costs,

Moore's Law not scaling, N20-N16-N10-N7-N5 costs to Apple, reticle limits,

chiplets, 2D going to 2.5D/3D, Cadence vs. Ansys, TSMC N3E FinFlex not

scaling, Qualcomm's ASP vs. Apple's costs, "chip design will go from a

few to many", "design democratization is coming..."

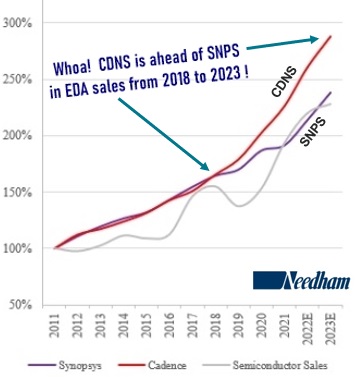

And then Charles Shi closed his talk with a shocking slide:

Zoom in and you'll see what Cooley (my added markings) saw:

Charles (very quietly) declared that CDNS (line in red) has been crushing

SNPS in pure EDA sales since 2018 -- and Charles predicted in his graph that

Anirudh will keep on crushing SNPS in EDA even in 2023!

That is, Charles Shi had quietly crowned Anirudh the King of Core EDA.

(And my spies tell me that Jay Vleeschhouwer's DAC'22 presentation also had

a similar slide showing CNDS EDA sales had bypassed SNPS EDA sales in

roughly the same time frame -- but I don't have a pic of that slide.)

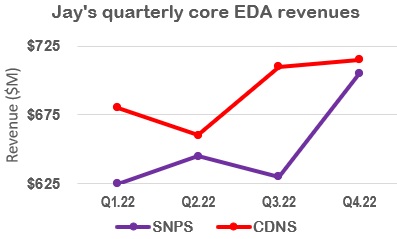

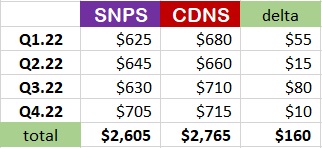

JAY'S CONFIRMATION: Since I couldn't get a screenshot of Jay's DAC'22 slides

on this, I did the next best thing -- I pawed through Jay's 2022 quarterly

reports on the individual Earnings Calls for SNPS and CDNS to see what Jay

saw for Core EDA revenues (i.e. no IP, no HW, just SW) for each company.

SNPS 22Q1: :############################### $625M

CDNS 22Q1: :################################## $680M ($55M more)

SNPS 22Q2: :################################ $645M

CDNS 22Q2: :################################# $660M ($15M more)

SNPS 22Q3: :################################ $630M

CDNS 22Q3: :#################################### $710M ($80M more)

SNPS 22Q4: :################################## $705M

CDNS 22Q4: :#################################### $715M ($10M more)

So for FY2022, Jay saw CDNS $160M ahead of SNPS in core EDA revenues.

That is, Anirudh was 6% ahead of Aart in core EDA for 2022.

---- ---- ---- ---- ---- ---- ----

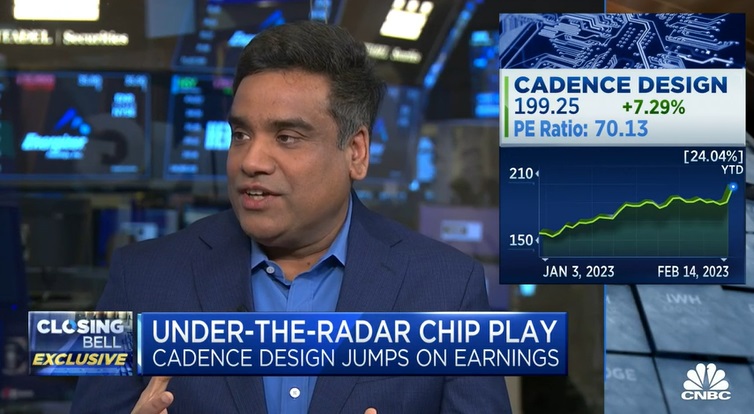

ANIRUDH'S KICKASS 22Q4: So then 10 days ago when CDNS reported it's kickass

FY22 earnings, Wall St. loved Anirudh because in FY22 his backlog grew

$1.4 billion to be $5.8 billion and Jay revised his CDNS FY23 estimate to

$4.039 billion (up 13%) with a 42% margin.

Cadence even got CNBC airtime for it's kickass 22Q4.

(click to view video)

But to be fair, Aart's SNPS also kicked ass in its FY22 with a whopping

$7.1 billion backlog (that didn't change significantly) and Jay revised

his SNPS FY23 estimate to be $5.786 billion (up 21%) with a 34% margin.

Charles and Jay gave both CDNS and SNPS each a "Buy" rating.

---- ---- ---- ---- ---- ---- ----

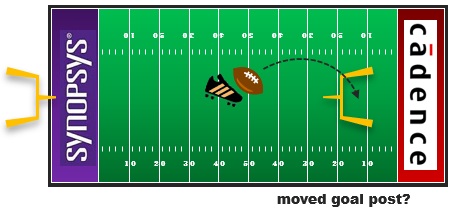

THE BUCKETS HAVE CHANGED: But in the recent SNPS 23Q1 Earnings Call that

was 3 days after the CDNS call, Aart's new CFO decided to totally rejigger

how SNPS reports its 2023 earnings. What SNPS revenues were put into

exactly what accounting bucket was totally changed ...

... so now Jay and Charles and the other Wall St. guys (and Cadence) have to

do a massive reassessment of all these newly reported terms (and their exact

definitions) to see how 2023 revenues compare to the prior 2022 revenues.

The cynical me would see this as SNPS sneakily moving the CDNS goal post to

the 25 yard line to gain an advantage against CDNS.

But the more optimistic me sees this as the new SNPS CFO trying to bring in

common sense (and well intended) changes of definitions to benefit everyone.

Either way, when your reporting buckets change, it creates a few quarters

of confusion making it next to impossible to compare the prior 2022 numbers

to these new 2023 EDA revenue numbers.

---- ---- ---- ---- ---- ---- ----

THE BIG PICTURE: So we won't know for a few quarters if Anirudh gets to keep

his "Core EDA crown" in 2023 until these new definitions are worked out.

But the big picture is 15 years ago when Mike Fister and four of his VPs

all resigned on the same day from CDNS back in 2008, Fister left CDNS in

a smoldering ruins -- and Aart's SNPS was the undisputed King of All EDA.

To go from absolute fiasco back then ... to today where CDNS is the King

of 2022 Core EDA and we're puzzling out if it's still King in 2023 ...

... in the big picture THAT is a solid "win" for Anirudh.

Editor's Note: do you know how difficult it is to find a horse

race pic where one horse is 6% ahead of the other horse? - John

---- ---- ---- ---- ---- ---- ----

"Growth contest between SNPS and CDNS is still a tie.

Investors like to ask us: between SNPS and CDNS, which one will

grow faster over the longer term? Our answer has consistently

been "it is hard to tell". The SNPS print tells us that SNPS' EDA

growth may be showing signs of underperformance, but SNPS' higher

mix and stronger growth of IP is lifting its overall growth to

a simliar level as CDNS.

Over a longer term, both companies should do similarly if not

equally well."

- Charles Shi, SNPS 2Q22 Needham report (05/19/2022)

Join

Index

Next->Item

|