( ESNUG 551 Item 2 ) -------------------------------------------- [06/02/15]

Subject: 317 engineers on today's SPICE use vs. their future SPICE use

> Now the CDNS/BDA lawsuit is settled and both companies' newly announced

> SPICE simulators have had 6 months to harden, for 2014 I predict the

> following shakeups in the SPICE market with...

>

> - Amit Gupta of Solido Design

> http://www.deepchip.com/items/0537-07.html

From: [ Amit Gupta of Solido Design ]

Hi, John,

Here's where our survey of 317 engineers compared today's current SPICE use

vs. the SPICE user's perception of the simulators. (I know this sounds like

marketing B.S., but perception surveys are quite helpful in seeing how an

EDA vendor is doing as compared to its rivals.)

---- ---- ---- ---- ---- ---- ----

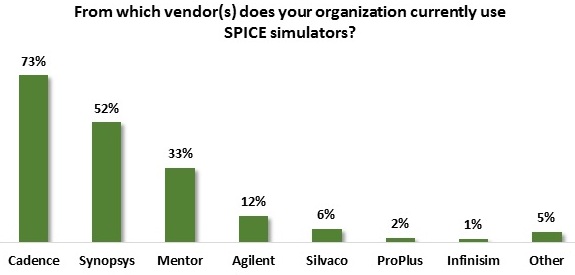

WHAT SPICE USERS ARE USING TODAY

Below are the relative vendor use proportions. This often differs from SPICE

market share because market share is based on the annual dollar amounts on

SPICE licenses sold. This question here is on what the SPICE users are

actually using now; not on the dollars they spent on SPICE that year.

All of Mentor's numbers include Eldo, BDA AFS, and a bit of Tanner T-Spice.

The major change is Mentor. Wally and Greg have been aggressively buying

custom IC design market share. I estimate that over the last 14 months

Mentor has grown from less than 5 percent SPICE customer use with Eldo, to

a healthy 33 percent from picking up BDA (and to a lesser degree, Tanner).

AND WHERE FUTURE SPICE SALES WILL BE

Knowing from our earlier survey question that 26% of groups will either be

evaluating or adding new SPICE simulators in the next 12 months, this SPICE

user perception data tells us where future SPICE sales will most likely be.

It's important to know that SPICE use is broken down by user segments. I

used to talk about them as these four niches:

- memory designs

- std cell libraries

- full custom digital

- pure AMS/RF

We used to break out AMS/RF from custom digital, but we're seeing that these

designers use pretty much the same tool flows -- so now I put AMS/RF/custom

digital into one merged segment.

---- ---- ---- ---- ---- ---- ----

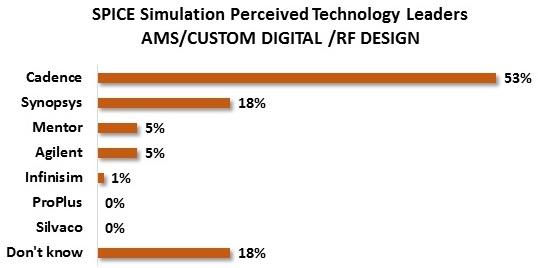

AMS, CUSTOM DIGITAL, RF DESIGN

Not surprisingly, Cadence is still perceived as the technology leader in

analog/mixed-signal, custom digital, and RF SPICE simulation -- with 53%

citing them as the technology leader.

I suspect this stems from the fact that Cadence Virtuoso and ADE has close

to 80% market share in the full custom and AMS design/layout tool market.

And although Synopsys has an 18% second place here, it's NOT from Aart's

Custom Designer tool -- which we are not seeing amoung the first tier

customers -- but from prior full custom SPICE market penetration by the

SNPS Avanti HSPICE and SNPS Magma FineSim SPICE simulators.

I expect Lip-Bu to keep dominating in the AMS/CUSTOM/RF SPICE niche, but

Keysight to start winning RF market share now that it has fully spun out

from Agilent, and Wally to gain with BDA AFS.

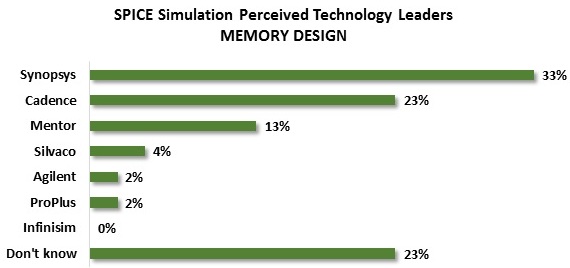

MEMORY DESIGN

Because memory cells are highly repetitive, their SPICE simulations can use

this to get far better speed/accuracy/capacity than general SPICE tools.

The other thing is memory designers are very fickle, they're always picking

the best SPICE simulator for the process and node they're on -- which is

why memory SPICE is the one to win. If you win memory, sales in the other

niches readily follow.

"SPICE is interesting in that you enter through memory; it's the

most unforgiving market there is. Zero tolerance. You gotta

have the best tool or they toss your tool out. Memory designers

have no loyalty to any SPICE vendor. This why Synopsys has 9

different SPICE simulators."

- Gary Smith during the DAC'14 Troublemakers Panel

Aart does well in memory SPICE because he acquired 6 different SPICE flavors

to offer memory designers. Magma FineSim does well, Aart buys it, and then

he keeps those FineSim users happy after the acquisition. Same with Avanti

and Nassda. But notice that SNPS only has 33% compared to CDNS 23% -- not

a big lead there -- plus 23% saw "no one" as a tech leader in memory SPICE.

The CDNS 23% here comes from buying the Altos memory characterization tools

plus their recent CDNS Spectre XPS launch (also focused on memory design.)

The fact that CDNS Spectre XPS benchmarked well against SNPS HSPICE at 16FF

in ESNUG 547 #3 shows how successful their tool is in memory design. Prior

to these two CDNS actions, I think Lip-Bu's share of memory SPICE leadership

was similar to Silvaco's small 4% number.

In addition, Wally's 5% leadership in memory SPICE today was actually 0.1%

when he only had Eldo. That 5% jump is purely from MENT buying BDA which had

launched AFS Mega targeted for memory designs 2 years ago -- not from Eldo.

The customer benchmark of BDA AFS Mega vs. SNPS Finesim Pro plus SNPS HSIM

for SRAMs in ESNUG 535 #3 confirms this.

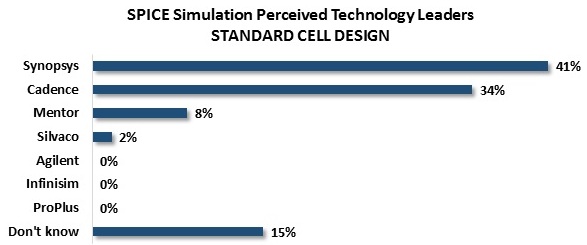

STD CELL DESIGN

If you compare the data for memory design leadership (above) and std cell

design leadership (below) you'll see that

even though they're two distinct SPICE design niches -- almost all of the

same comments apply. SNPS leads with HSPICE and FineSim, and CDNS jumped

up from buying the Altos std cell characterization tools.

The only technical difference is memories are lots of repeat instances of

a few well designed cells. Std cell libs are a mix of many different small

"building blocks" used to make digital chips.

---- ---- ---- ---- ---- ---- ----

SNPS SPICE UNDER ATTACK

> With Synopsys annexing Magma FineSim through the recent acquisition,

> Synopsys will monopolize custom digital, memory, and std cell. Aart

> will recapture his estimated $70 million/year in lost business to

> Magma, and with Magma's history of price cutting and commoditizing

> now eliminated... all SPICE prices will go up dramatically.

>

> - from http://www.deepchip.com/items/0496-07.html

If you look at the SPICE Wars post in ESNUG 496 #7 that analyzed how Aart's

buying Magma would raise all SPICE prices back in 2011, what I personally

see from our own customers and from this survey is that CDNS and MENT are

taking advantage of this by aggressively going after SPICE niches that

SNPS or LAVA had earlier dominated.

Why I say this is if this survey had been done 5 years before, CDNS and MENT

would have been in 2% leadership roles in memory and std cell -- with SNPS

easily crushing both -- instead CDNS and MENT are now serious challengers

to SNPS/LAVA/Avanti/Nassda SPICE in these two niches.

The other thing that backs this is how in each SPICE niche (18%, 23%, 15%)

had said "no one" was the technology leader in that niche -- meaning that

a good portion of SPICE buyers see their next SPICE purchase being anyone's

game right now.

- Amit Gupta

Solido DA Saskatoon, Canada

---- ---- ---- ---- ---- ---- ----

Related Articles:

317 engineers surveyed on general SPICE use & SPICE requirements

317 engineers on today's SPICE use vs. their future SPICE use

And the variation part of Amit's 317 engineer SPICE survey...

---- ---- ---- ---- ---- ---- ----

Join

Index

Next->Item

|

|